What Are Business Bridge Loans

& How Do They Work? Complete Guide

Looking for Business Financing?

Apply now for flexible business financing. Biz2Credit offers term loans, revenue-based financing, lines of credit, and commercial real estate loans to qualified businesses.

Set up a Biz2Credit account and apply for business financing.

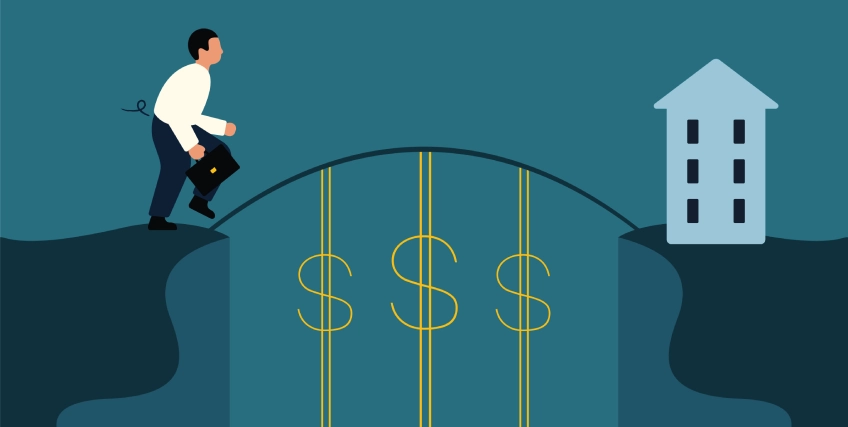

Keeping a business up and running is all about cash flow. Companies often know they'll have access to money somewhere ahead but that doesn't solve quick cash needs. This may include accounts payable to payroll. This is where a business bridge loan walks in. It is a short-term funding product that helps companies to grab time-sensitive opportunities or manage important transactions without delays. These loans are important for businesses that need to move quickly, such as those involved in mergers and acquisitions, commercial property development, or companies awaiting the closing of long-term funding. While often used by commercial entities, the concept is similar to a swing loan or a residential bridge loan.

Unlike conventional lenders, bridge lenders focus more on asset value and exit strategy than credit history. They do not need laborious, technical application and approval processes. In line with it, this page explains what a bridge loan is, its uses, eligibility criteria, pros and cons, alongside financing options and loan approval tips.

What is a Business Bridge Loan & How Does it Work?

A business bridge loan is a type of short-term financing solution, offering quick access to funds to cover functional expenses. This is until a business secures more permanent, long-term funding or completes a major transaction, such as an asset sale. They are effectively used for 'bridging finance gaps' in a company's cash flow during transitional or seasonal periods.

Key Characteristics of Bridge Loans

- Short-Term Duration: Typically ranges from a few months.

- Quick Funding: Features a quicker application and decision process compared to traditional long-term loans.

- High Interest Rates and Fees: Due to speed and risk, bridging loan interest rate is generally higher and additional fees, such as origination and legal costs, may be needed.

- Collateral Requirements: Most bridge loans are secured, needing assets like real estate or business inventory as collateral to provide security for the lender.

- Clear Exit Strategy: A well-defined plan for repayment, such as proceeds from a long-term loan, an IPO, or property sale, is required by lenders.

Common Business Bridge Loan Uses

- Mergers and Acquisitions (M&A): Securing quick funds to act quickly on time-sensitive opportunities, before permanent financing arrives.

- Expansion Costs: Funding the opening of a new location or other growth initiatives while waiting for long-term capital.

- Working Capital: Covering temporary cash flow shortfalls for operational expenses, like clearing out payroll, paying rent, or updating inventory purchases.

- IPO Expenses: Covering flotation costs (underwriting, stock exchange fees) before an initial public offering (IPO) is complete and capital is raised.

- Property Development/Renovation: Buying new property for renovation, to meet the requirements for a traditional commercial mortgage or sale.

Financing Options: Business Bridge Loan

When applying for a business bridge loan, it is important to explore and understand the types of financing options that are available. This helps businesses choose the most-suited bridge loan, which comes with comfortable bridging finance rates and matches overall expectations. Here are the key financing options, when choosing a bridge loan:

Closed Bridge Loans

These loans have a predetermined repayment date and a clear, documented exit strategy, such as an approved long-term mortgage or a confirmed property sale. This defined term makes them less risky for lenders and can result in more favorable interest rates for the borrower.

Open Bridge Loans

Offering more flexibility, these loans do not have a fixed repayment date or a fully defined exit strategy at the time of funding. Due to the increased risk for lenders, they typically come with higher interest rates and may require interest to be deducted upfront.

First Charge Bridge Loans

In this type, the bridge lender holds the primary claim or "first charge" on the collateral. In case of a default, this lender is repaid first before any other creditors. This increased security for the lender often results in lower interest rates.

Second Charge Bridge Loans

This loan is secured by a secondary claim on a property that already has an existing mortgage or first charge. The second charge lender is only repaid after the first charge lender has recovered their funds in a default scenario, making them riskier and typically more expensive for the borrower.

Regulated vs. Non-Regulated

The primary difference here is consumer protection. Regulated bridge loans are used for personal residences and are subject to stricter rules set by gov bodies like the Financial Conduct Authority (FCA). Non-regulated loans are typically for commercial property or investment purposes and may have fewer restrictions.

Alternatives to Bridge Loans

Small Business Administration (SBA) CAPLines Program

This is an umbrella program designed to help small businesses meet short-term and cyclical working capital needs. The lines of credit within this program are often tied to specific business cycles, like seasonal sales or specific contracts, and thus serve to bridge those particular funding gaps.

Business Line of Credit (LOC)

This acts like a flexible credit card for a business, allowing it to borrow funds up to a set limit, repay the amount, and borrow again as needed. It is a revolving source of cash, that may be used for bridging unexpected or temporary working capital gaps. The interest is paid only on the amount actually used, not the full limit.

Accounts Receivable Factoring (Invoice Factoring)

This alternative solves the problem of slow-paying customers by allowing a business to sell its unpaid invoices to a third-party company (a "factor). This is done at a small discount for quick cash. The "factor" then takes over the responsibility of collecting the full payment from the customer. This method is not technically a loan and is known for swiftly turning outstanding invoices into working capital, to stabilize cash flow without new debts.

Short-Term Term Loan

It is a simple lump-sum loan, given all at once, which the business repays in fixed instalments over a brief period. This alternative is suited for funding a specific, one-time, urgent purchase, such as equipment or paying for an unexpected business expense. Under this solution, the business has a clear, predictable timeline to generate the revenue needed for repayment.

Hard Money Loans

These are highly specialized, short-term funding provided by private investors or non-bank lenders. They are characterized by a lending decision based almost entirely on the value of the asset serving as collateral, rather than the borrower's credit or financials. While acting as a quick bridge loan, they usually come with higher interest rates due to the speed and risk profile.

Home Equity Line of Credit (HELOC)

Another common alternative to a bridge loan; however, it is fundamentally different from a commercial bridge loan. While a bridge loan is a lump-sum, short-term loan, a HELOC functions as a revolving line of credit, secured by the borrower's personal residence. This allows a business owner to repeatedly draw funds up to a set limit, repay the amount, and borrow again as needed. Interest is only paid on the amount used. Although majorly a consumer product, the flexibility and relatively lower interest rates compared to a standard bridge loan make it a feasible option for a business owner.

Eligibility Criteria When Applying For a Bridge Loan

Eligibility criteria for a business bridge loan are typically stricter and more focused on the collateral and the exit strategy, than traditional long-term financing. Lenders evaluate three major elements: the business itself, the borrower, and the specific transaction. Check the tables below to get a fair idea of common business bridge loan eligibility requirements:

Business and Borrower Eligibility

| Criteria | Details and Requirements |

|---|---|

| Financial Health | Lenders commonly require revenue and strong cash flow to cover the interest-only payments. A solid record of profitability is often required, though flexibility exists, if the collateral is very strong. |

| Credit Score | The business owner's personal credit score (FICO) and the business credit score are both checked. Lenders prefer solid scores, though private hard money lenders may accept lower scores, if the collateral is sufficient. |

| Time in Business | Most lenders prefer businesses that have been operating for at least 1 to 2 years, to ensure stability and a consistent revenue track record. |

| Debt Service Coverage | The business must show it can cover the monthly interest payments. Lenders often look for a Debt-to-Income ratio or a high Debt Service Coverage Ratio to ensure short-term creditworthiness. |

| Management Experience | For commercial real estate bridge loans, the borrower or management team should have relevant experience managing or flipping similar properties. This shows proof of competence, in executing the exit strategy. |

Collateral Eligibility

| Criteria | Details and Requirements |

|---|---|

| Clear Exit Strategy | Lenders require a clear, documented, and highly-practical plan for repaying the loan when it matures. Common exit strategies include:

|

| Collateral Quality | The loan is secured by valuable assets, most commonly commercial or investment real estate or high-value equipment. The collateral must be readily sellable. |

Tips: Applying for a Business Bridge Loan

Applying for a business bridge loan in the U.S. market requires a focused, multi-stage approach, centred on showing a low-risk repayment plan and asset security. The process demands meticulous pre-application preparations; specifically defining a clear exit strategy and assessing collateral. This is followed by organized execution of the application, with detailed documentation, and concluding with responsible post-loan management. Listed below are some common yet crucial tips to keep in mind when trying to qualify for a bridge loan:Pre-Application Preparation

| Focus Area | Key Action |

|---|---|

| Clear Purpose and Exit Strategy | Define the specific, short-term need for the capital. A detailed "exit strategy" must be presented, showing exactly how the loan will be repaid. |

| Financial Health Assessment | Lenders evaluate the business's financial statements (tax returns, P&L, bank statements). Maintaining a debt-to-income (DTI) ratio of 50% or lower is generally advisable to show financial stability. |

| Collateral Readiness | Most bridge loans are secured. Gathering and appraising high-value collateral (e.g., commercial real estate, equipment) is essential. The value of these assets determines the maximum possible loan amount (Loan-to-Value ratio). |

| Lender Research | Bridge loans often come with high interest rates and hefty upfront fees. Shopping around and comparing multiple offers from banks, credit unions, and specialized private lenders helps secure favorable terms. |

Application Process Execution

| Focus Area | Key Action |

|---|---|

| Detailed Business Plan | The plan must mention a stable business history, consistent revenue , and strong cash flow. It must also outline the proposed use of the loan funds and the detailed repayment strategy. |

| Meticulous Documentation | All required paperwork must be readily organized for a smooth process. This includes financial statements, tax returns, appraisals for proposed collateral, proof of ownership, and management team credentials. |

| Responsiveness | The bridge loan process is often rapid, sometimes completing within days. Providing any additional information promptly upon request from the lender is important towards avoiding approval delays. |

| Negotiate Terms | Upon receiving a loan offer, the terms should be reviewed carefully. Negotiating aspects like interest rates, repayment schedules, and fees is often possible, and professional advice may be helpful before signing. |

If Approved:

| Focus Area | Key Action |

|---|---|

| Cash Flow Management | Even with common interest-only monthly payments, the associated costs must be linked to the business's ongoing cash flow to prevent cash strains. |

| Contingency Planning | If the planned exit strategy is at risk of missing its deadline, the business must explore refinancing options with other lenders. Existing bridge facilities are rarely rolled over or extended by the original lender. |

| Maintain Transparency | Keeping the lender consistently updated on the progress toward the exit strategy is important for successfully managing short-term loans. |

Business Bridge Loan: Advantages & Drawbacks

A business bridge loan offers an important trade-off for companies in the U.S. market; they provide unparalleled speed and flexibility to seize time-sensitive opportunities. However, this comes at a financial cost, as these loans are characterized by substantially higher interest rates and fees. Therefore, the borrower must have a meticulously planned and reliable exit strategy, to avoid the severe penalties associated with the short term and high cost of the debt. Here are a few pros and cons of a bridge loan:

Pros

Speedy Access to Capital

Bridge loans offer a significantly quicker funding than traditional bank loans, which may take months. This allows a business to seize time-sensitive opportunities, such as bidding on a property auction or getting a high-value contract.

Flexible Underwriting

Lenders often prioritize the "hard" value of the collateral and the exit strategy, over the borrower's credit score. This is important for businesses with complex finances or those that need financing quicker than a bank's lengthy underwriting process allows.

Enables Non-Contingent Deals

In competitive real estate markets, a bridge loan allows a buyer to make an offer without a financing contingency. This increases the likelihood of the seller accepting the bid. This is an important competitive advantage for investors.

Interest-Only Payment Options

Many bridge loans offer interest-only payments during the term. This minimizes the monthly cash burden on the borrower while they complete the project or await the sale/refinance.

Finances Non-Stabilized Assets

Traditional lenders often refuse to finance properties that require significant renovation or are currently vacant. Bridge loans are specifically designed to fund these "value-add" opportunities.

Cons

Higher Interest Rates and Fees

Bridge loans may be riskier due to their short terms. Consequently, they carry significantly higher interest rates and hefty origination/closing fees, making them a costly debt.

The Need for an Exit Strategy

The loan's term is short (typically 6 to 24 months), requiring a clear, documented repayment plan. If the expected event, like a long-term loan closing or asset sale, is delayed, the borrower faces a lot of pressure and penalty fees.

Risk of Default and Foreclosure

As these loans are heavily reliant on collateral, failure of the exit strategy can lead to a forced sale of the asset. This may be done by the lender to recover their capital; thus, it creates high financial risk for the business.

Managing Multiple Debts

In real estate, a business may temporarily be required to manage payments on the existing mortgage, the new bridge loan, and potentially the new long-term financing. This creates severe cash flow strain.

Potential for Closing Costs Duplication

Since the bridge loan is a temporary solution, the business must pay closing costs/origination fees twice: once for the bridge loan and again for the subsequent long-term, permanent financing.

Business Bridge Loan: Expansions & Transactions Without Delays

A bridge loan helps a business move through short-term cash gaps while awaiting long-term capital, a major transaction, or incoming revenue. It often supports a down payment on a project, covers operational needs, or stabilizes cash flow until the final balloon payment at the end of the term. The way bridge loan terms work is simple on paper: funds arrive quickly, interest is higher, and repayment depends on a clear exit plan, such as refinancing, asset sale, or securing a new mortgage on commercial property. Lenders focus on the business's collateral, the home's value equivalent in commercial assets, and the LTV that shapes approval conditions.

From a business perspective, the cons of bridge loans lie in their cost and tight timelines, which means loan officers and mortgage lender counterparts must review risks carefully. Companies may also compare options like an FHA-style backed facility for property, or a home equity loan equivalent in commercial lending, before deciding. When used wisely, bridging finance may support expansion and transactions without delays. But it demands strong cash flow planning and readiness for every mortgage payment or refinancing step that follows. So, when looking for a bridge loan, it is important to review all terms and conditions carefully, to avoid surprises later.

Trusted by Thousands of Small Business Owners in America.**

Simply because we get what you go through to build a business you believe in.

**Disclaimer: All stories are real, as told by real business owners. Customers do not receive monetary compensation for telling their stories.

From One Entrepreneur to Another: We Get You

We understand what's behind building a business you believe in.

All stories are real, as told by real business owners. Customers do not receive monetary compensation for telling their stories.

Articles on Small Business Bridge Loans

Need Cash in 48 Hours? Fast Bridging Loans Could Be the Answer

Most startup owners understand the importance of selecting the right business credit card for new businesses. It's more than just swiping a card.

Why Bridge Financing in Real Estate Might Be Your Best Bet in 2026

The real estate market in 2025 is moving at full speed. Buyers are acting fast, and properties are closing quicker than ever. With this speed

Understanding a Bridge Loan for Business

In the dynamic world of business, timing can be everything. Whether you're trying to seize a new opportunity, manage cash flow, or close a gap

Bridge Loans vs. Business Lines of Credit: Which is Better for Temporary Gaps?

Small business owners deal with many challenges that can cause gaps in cash flow. From payment delays from customers to seasonal downturns

Is a Bridge Loan Right for Your Expansion? A 2026 Checklist

Whether you are looking to acquire a new home, snap up prime commercial real estate...

Bridge Loan Rates: 2026 Market Update

Bridge loan rates are one of those things that sound simple until you actually need one.

Bridge Loan Interest Rates vs. Hard Money: What’s the Real Difference?

Real estate is a high-stakes sector where you need to have funds available right away to...

How Bridge Loans Help Entrepreneurs Quickly Secure a Small Business Purchase

Buying a business isn’t just about the right asking price. It’s also about timing. Entrepreneurs often find themselves competing with

Hard Money vs. Bridge Loans What’s the Best Option for Real Estate Investing

Apart from traditional mortgages, you can also choose from asset-based loans, such as bridge loans and hard money loans

FAQs About Bridge Loan

1. When should a small business consider applying for a bridge loan?

A small business may consider a commercial bridge loan to cover temporary cash gaps or to make use of time-sensitive opportunities, when waiting for long-term financing. To figure out the ideal time, business owners need to review their business plans, funding requirements and purpose, eligibility criteria alongside repayment ability.

2. Are bridge loans expensive?

Business bridge loans generally have higher interest rates and fees, in comparison to traditional mortgages, due to their short duration and increased lender risks.

3. How to qualify for a business bridge loan?

To qualify for a bridge loan, borrowers typically need a strong credit score, a low debt-to-income ratio, assets to put up as collateral, and a loan repayment strategy. Lenders may typically require significant equity in the current property as well, to ward off risks and ensure the borrower has sufficient financial stake in it. Checking all lender terms and conditions before applying, increases qualification chances.

4. Who offers bridge loans in the USA?

A business bridge loan is a common and established short-term financing tool, particularly in real estate and corporate finance. It is offered through SBA-related programs, traditional banks, credit unions, specialist bridging lenders, and private capital firms.

5. What are the risks of a bridge loan?

Bridge loans offer quick, short-term funding but carry significant risks, due to their speed and convenience. The primary risks include high interest rates, the potential for default and loss of collateral, and the challenge of managing a short repayment window.

Frequent searches leading to this page

Term Loans are made by Itria Ventures LLC or Cross River Bank, Member FDIC. This is not a deposit product. California residents: Itria Ventures LLC is licensed by the Department of Financial Protection and Innovation. Loans are made or arranged pursuant to California Financing Law License # 60DBO-35839